Expense optimization across the year

A recognized expense doesn't save you 100% of the amount; it saves you your marginal tax rate on that amount. That's the difference between thinking about expenses as "I'm spending so I'm saving" vs. "this is an investment in my tax envelope." This chapter explains how to time expenses by your marginal rate and how to identify expenses that are genuinely recognized.

The first question: what's your marginal rate

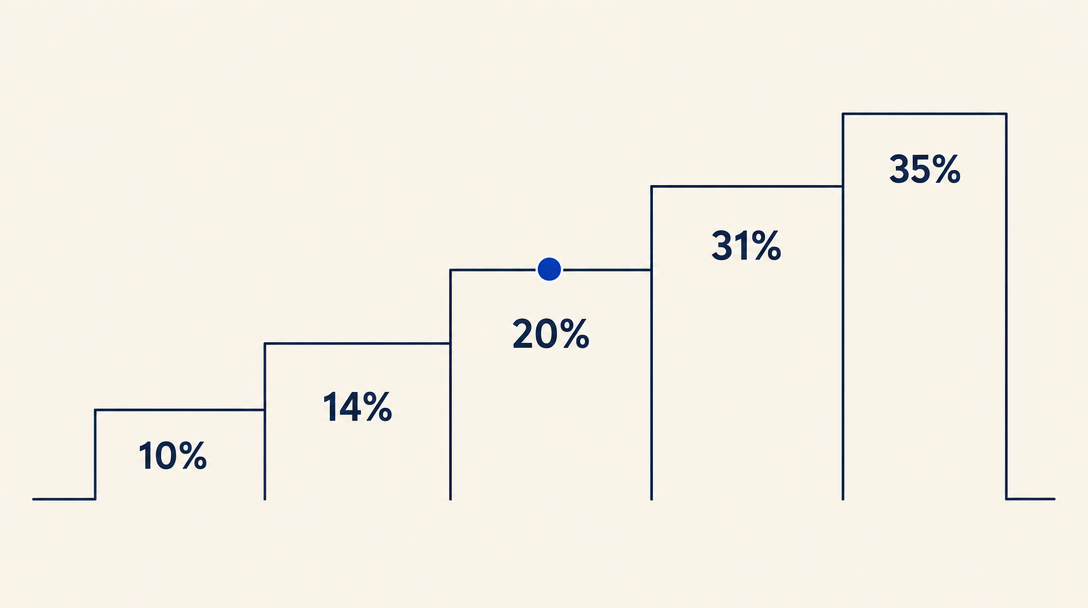

Before deciding on any expense, you need to know your marginal tax rate. That's the tax percentage that will apply to the next shekel you earn. Find it on last year's form 1301, or compute it from the 2026 brackets:

| Annual taxable income (₪) | Marginal rate |

|---|---|

| Up to 84,120 | 10% |

| 84,121 to 120,720 | 14% |

| 120,721 to 193,800 | 20% |

| 193,801 to 269,280 | 31% |

| 269,281 to 560,280 | 35% |

| 560,281 to 721,560 | 47% |

| Over 721,560 | 50% (plus 3% surtax) |

A recognized expense of ₪1,000 saves you:

- ₪140 if your marginal rate is 14%

- ₪200 at 20%

- ₪350 at 35%

- ₪500 at 50%

This gap is the core of expense optimization.

Categories of recognized expenses

1. Section 17, home office. If you work from home, you can deduct a proportional share of household expenses (electricity, water, internet, home insurance) based on the percentage of the room used as office. Example: 100 sqm apartment, 12 sqm workspace, deduct 12% of those expenses. The deduction must be documented with a defensible calculation. Be aware: arnona and mortgage interest for a residential property used as home office are contested positions. Arnona is generally only deductible if the room is classified for business arnona (which then raises the arnona itself), and an aggressive home-office deduction is one of the common triggers for a books audit. If you're claiming more than the basic utilities split, get a CPA review first.

2. Equipment and depreciation. Personal computers depreciate at 33% per year per the Income Tax Regulations (Depreciation). Other equipment depreciates at the rates set in the regulations: 25% for "other computers", 7%-25% for furniture and fixtures, depending on type. Equipment items under ₪2,000 may be fully expensed in the year of purchase under the accelerated-depreciation rules. Annual-subscription professional software is fully expensed in the year.

3. Vehicle. If the vehicle serves both work and personal use, 45% of expenses (fuel, insurance, service, depreciation) are recognized under the Income Tax Regulations for vehicles under 3.5 tons. That's the standard rate for self-employed and requires no proof of business usage. The alternative is "total expenses minus the imputed personal-use value (shavi shimush)", whichever is higher; in practice 45% is what most freelancers claim.

4. Professional development. Courses, books, conferences, professional service subscriptions. Must be "within the specific profession" of your business, not a new field you're exploring.

5. Professional insurance. Professional liability, equipment property insurance, self-employed income insurance (under conditions).

6. Supplier services. Accountant, tax advisor, lawyer for business matters, cloud and software services, other freelancers you pay (they must issue you an invoice).

7. Bituach Leumi self-employed contributions (52% deductible). Under Section 47A of the Income Tax Ordinance, half of what you paid in self-employed Bituach Leumi contributions (specifically 52%) is deductible from your taxable income. For most freelancers this is one of the largest single deductions, often ₪5,000-₪15,000 per year, and it's a common omission for solo filers who don't know it exists.

The magic of keren hishtalmut for self-employed

Keren hishtalmut for self-employed is one of the most powerful tools in your tax framework. Two separate caps apply in 2026, and most freelancers confuse them:

- Deductible-contribution cap: 4.5% of annual income, computed on income up to ₪293,397. That works out to a maximum of ₪13,203 per year you can deduct from taxable income.

- Capital-gains-exempt deposit cap: a separate, higher limit of ₪20,566 per year. Deposits up to this ceiling enjoy capital-gains-tax exemption when you withdraw after 6 years. Deposits between ₪13,203 and ₪20,566 give you the capital-gains exemption but no income-tax deduction.

- After 6 years the money is released. Amounts deposited up to the ₪20,566 capital-gains-exempt cap come out free of the 25% capital gains tax on the fund's returns.

The contribution must be made by December 31 of that tax year. If your marginal rate is 35% and you contributed the full deductible ₪13,203, you saved ₪4,621 in tax for the year. If you went up to the ₪20,566 capital-gains-exempt cap, the additional ₪7,363 doesn't reduce this year's tax bill but its future returns won't be taxed at 25% on withdrawal. The total return on the contribution over 6 years is roughly 35% to 50%, before the fund's own investment return.

Section 47, self-employed pension

Pension contributions for the self-employed receive two tax benefits, both with caps tied to the average wage (currently ₪9,700 per month of uninsured salary, indexed annually):

- A deduction under Section 47, up to 11% of uninsured income (capped on the ceiling above).

- A 35% credit under Section 45a on an additional 5% of uninsured income.

The deduction reduces taxable income, so it's worth more if your marginal rate is high. The credit gives back a flat 35% of the contributed amount regardless of bracket, so it's relatively more valuable if your marginal rate is low. Most freelancers want both, in the right order. Your accountant or the matching skill will compute the optimal split for your income level.

Timing within the year

Expense timing affects its value. If you see year-end will land in a higher bracket than next year (a big project closed), it pays to push expenses to next year and pull invoices into this year. If reversed (next year forecasts higher income), pull expenses into this year.

The simplest rule: spend in the year your marginal rate is highest.

The most common mistake

The classic mistake: classifying non-recognized expenses as recognized. Common examples:

- Business meals that weren't business (you ate alone or with family)

- Clothes "for client meetings" that aren't formal uniforms

- Household appliances that serve work but not primarily

- Client gifts above ₪230 per person per year (2026 indexed ceiling per the Income Tax Regulations on deduction of certain expenses; above that, not recognized). Additionally: the gift must carry permanent business branding/logo. Cash, gift cards (tlushei kniya), and generic ungifted gifts are not deductible at any amount.

If an accountant or Reshut HaMisim audit comes back and disqualifies an expense, you'll pay not just the tax difference but interest and linkage differences, sometimes a penalty too. Better to be conservative.

Skills to install for this chapter

- Israeli Bank Connector (

israeli-bank-connector), for automatic categorization of all expenses from your bank account, saving hours of manual tagging at year-end. - Israeli Pension Advisor (

israeli-pension-advisor), for calculating optimal contributions to keren hishtalmut and pension by your marginal rate.

What you should know after this chapter

- Your marginal rate and how it affects the value of every recognized expense

- The 6 main expense categories allowed for self-employed in Israel

- The priority order between keren hishtalmut, pension, and operating expenses

- When to pull and when to push expenses between two tax years

The next chapter covers end-of-year strategy: decisions made in October-November-December that affect the April tax bill.

Want to keep reading?

Sign in to unlock the rest of the course and track your progress.